Globale Broker-Regulierungsanfrage-App

WikiFX

Deutsch

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Bearish News at Market Lows, Bullish News at Market Highs

Zusammenfassung:A timeless sentiment indicator in the stock market: “Bearish news at the lows, bullish news at the highs.” The classic market adage says, “Markets are born in despair, grow in skepticism, mature in op

A timeless sentiment indicator in the stock market: “Bearish news at the lows, bullish news at the highs.” The classic market adage says, “Markets are born in despair, grow in skepticism, mature in optimism, and die in euphoria.”

Current Optimistic Headlines Seen by Investors

Trump extends the U.S.–China reciprocal tariff deadline by another 90 days.

Possible ceasefire in the Russia–Ukraine war; Trump to meet with Putin on August 15.

U.S. corporate stock buybacks reach $983.6 billion, on track to surpass $1.1 trillion this year.

The next Federal Reserve Chair nomination to be announced soon.

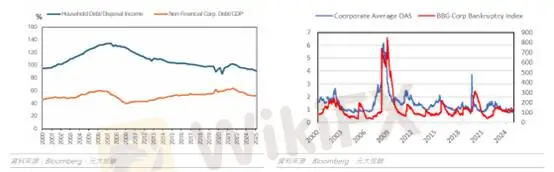

U.S. Household and Corporate Balance Sheets Remain Solid

(Chart 1: Household and Corporate Debt-to-Income/GDP Ratios; Source: Yuanta Securities Investment Consulting)

The Emerging Risk: Government Interest Payments

(Chart 3: U.S. Net Interest Payments; Source: Morgan Stanley)

Conclusion

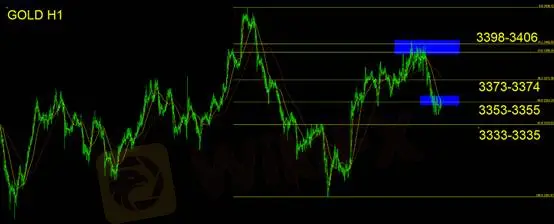

Gold Technical Outlook

Above $3,333–$3,335: Expect a broad sideways consolidation.

Below $3,333–$3,335: Could signal the start of a broader downtrend.

Compared with the fear-driven sentiment and negative headlines in April, todays market is trading at higher levels with increasingly optimistic news flow. We continue to advise investors to remain cautious—very cautious.

As of Q1 2025, U.S. household debt stood at about 91% of disposable income, the lowest since 1998 and well below the 134.34% peak seen before the 2007 financial crisis. Corporate (non-financial) debt-to-GDP fell to 64% as of Q2 2022—near 2015 levels—indicating a steady improvement in corporate default risk metrics.

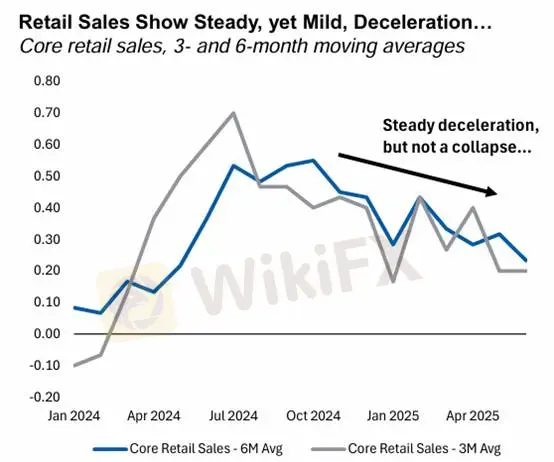

From both household and corporate perspectives, while equity markets are at elevated levels, we see no immediate signs of a market crash or an economic recession. However, retail sales data shows early signs of fatigue.

(Chart 2: 3-Month and 6-Month Moving Averages of Retail Sales; Source: Morgan Stanley)

In 2025, net interest payments are expected to consume 18.4% of federal revenue—a significant rise compared to historical norms, though in line with the previous peak in 1991. While we believe the U.S. faces minimal near-term refinancing risk, this trajectory is unsustainable. Fiscal consolidation and potential debt monetization could follow.

Trump‘s upcoming Fed Chair nomination is likely aimed at reducing the interest expense burden, which would, in turn, diminish Chair Powell’s influence.

")

We believe that any market correction is likely to be gradual, with pullbacks limited to the 5%–15% range. Given risk appetite trends and financial stability, there is little scope for a significant near-term rotation into safe-haven assets. Instead, a market pullback could trigger portfolio rebalancing into other asset classes.

Gold has held above the $3,000 mark for over a quarter. In the short term, prices have declined from the $3,400 level to $3,350. Based on Fibonacci retracement levels, the next key support to watch is $3,333–$3,335.

Our bias remains neutral to slightly bearish, with a suggested stop-loss of $25.

Support: $3,333–$3,335

Resistance: $3,353–$3,355 / $3,373–$3,374 / $3,398–$3,406

Risk Disclaimer: The above views, analyses, research, prices, or other information are provided as general market commentary and do not represent the views of this platform. All readers are solely responsible for their investment decisions. Please trade with caution.

Haftungsausschluss:

Die Ansichten in diesem Artikel stellen nur die persönlichen Ansichten des Autors dar und stellen keine Anlageberatung der Plattform dar. Diese Plattform übernimmt keine Garantie für die Richtigkeit, Vollständigkeit und Aktualität der Artikelinformationen und haftet auch nicht für Verluste, die durch die Nutzung oder das Vertrauen der Artikelinformationen verursacht werden.

WikiFX-Broker

Aktuelle Nachrichten

Disney-CEO Bob Iger über KI: So kann Künstliche Intelligenz das Streaming-Erlebnis verbessern

WikiFX

WikiFXWechselkursberechnung

USD

CNY

Aktueller Wechselkurs: 0

Bitte geben Sie den Betrag ein

USD

Konvertierbarer Betrag

CNY

Berechnen